Frequently Asked Questions

What are the Main Federal Income Tax Issues Associated with Aircraft Use.

There are three principal issues associated with private aircraft ownership. First is the ability to claim accelerated depreciation deductions and/or bonus depreciation. However, to do so the "qualifed business use" percentage for the aircraft determined under Internal Revenue Code ("IRC") Section 280F must be at least 50% (determined under either the flight by flight method (using either hours or miles) or the occupied seat method (using either hours or miles)). The "qualified business use" percentage must also be in excess of 25% determined by excluding certain flights for control persons. Second, you must determine the imputed income amount for personal use of the aircraft. Ordinarily, it is most advantegeous to use the SIFL method set forth in the IRS regulations to determine that amount. The SIFL method ordinarily produces an imputed income amount that is a fraction of the actual fixed and variable costs for the flight. Lastly, in the case of personal entertainment (for specified individuals as defined in Section 274) and commuting flights, you must determine the costs allocable to these flights. These costs generally may not be deducted under IRC Section 274, except (in the case of entertainment flights) to the extent of income recognized by the employee.

Standard Industry Fare Level (SIFL)

The U.S. Department of Transportation publishes SIFL rates for each six-month period (January 1 - June 30 and July 1 - December 31). These rates are used to determine the imputed tax value of non-business or personal travel aboard employer-provided aircraft under Internal Revenue Service Regulation Section 1.61-21(g). The SIFL amount is determined on a per-flight, per-person basis and generally reported to the responsible employee on IRS Form W-2 each taxable year. The value of a flight determined under the SIFL formula involves multiplying the SIFL cents-per-mile rates applicable for the 6 month period during which the flight was taken by the appropriate aircraft multiple provided in Treasury Regulation Section 1.61-21(g)(7) and miles (statute not nautical) traveled and then adding the applicable terminal charge.

What are the applicable SIFL Rates?

SIFL rates are published twice per year. The software automatically applies the correct SIFL rates for each flight and passenger entered (using the lowest rates permitted). For reference, attached are links to the semi-annual SIFL rates for recent periods:

- Historical and Current SIFL Rates from 1979 through June 30, 2024

- Rev. Rul. 2021-11 (SIFL Rates for January 1, 2021 -- June 30, 2021)

- Rev. Rul. 2021-19 (SIFL Rates for July 31, 2021 -- December 31, 2021)

- Rev. Rul. 2022-12 (SIFL Rates for January 1, 2022 -- June 30, 2022)

- Rev. Rul. 2022-19 (SIFL Rates for July 31, 2022 -- December 31, 2022)

- Rev. Rul. 2023-7 (SIFL Rates for January 1, 2023 -- June 30, 2023)

- Rev. Rul. 2023-19 (SIFL Rates for July 1, 2023 -- December 31, 2023)

Historically, only a single SIFL rate has been published for each six month period. However, due to the pandemic impacts, 3 different SIFL rates have been published for certain six month periods. The IRS has indicated that taxpayers may use any of the three rates when determining the value of flights.

Special SIFL Rules

- Children under the Age of Two Are not counted for SiFL purposes

- If fifty-percent (50%) or more of the seating capacity on an aircraft is occupied with employees traveling on business, no SIFL income is imputed for the personal travel of employees, spouses of the employee or their children on that flight.

Advanced SIFL Calculations

To learn more about calculating the applicable SIFL amount in varying circumstances or for more advanced SIFL Calculations, please see our comprehensive SIFL materials including an Advanced SIFL Calculator.

Public Company Reporting (SEC) Incremental Costs of Personal Flights for Named Executive Officers

Permitting an executive officer or director to use a company aircraft or company provided aircraft for personal use may require public disclosure of the incremental costs incurred as extra compensation under federal securities law. SEC Rules provide that the flights shall be valued on the basis of the aggregate incremental costs to the company. “Aggregate Incremental Cost” for personal use of non-commercial aircraft is generally thought to include any direct operating costs to the Company attributable to the personal use flight. In the case of personal use of fractionally owned Company aircraft, the direct operating costs would include: occupied hourly charge, fuel surcharge, Federal excise tax, landing, hangar and other airport fees, specialized catering fees, customs/immigration fees, ground transportation fees, passenger fees, and any flight-specific insurance costs.

Key Definitions

Tax and SEC accounting for aircraft use is complicated by the fact that each of the applicable provisions utilizes a different definition for the executive or employee traveling on the aircraft for personal use. Internal Revenue Code Section 280F (applicable for bonus and accelerated depreciation) focuses on business travel by 5% owners and related persons. Internal Revenue Code Section 274 requires a determination whether an executive or employee is a Specified Individual. Utilization of Standard Industry Fare Level (SIFL) rates to impute income to executives and employees requires a determination of whether the executive or employee is a "Control Person". Reporting of incremental costs for a trip for SEC reporting purposes requires a determination of whether the executive is a Named Executive Officer. Summarizes of these terms is set forth below:

- Control Person. Control Employees are board members, shareholders, elected officers and employees compensated among the top 1% of all paid employees.

- Specified Individual. Any individual who is subject to the requirements of Section 16(a) of the Securities Exchange Act of 1934 with respect to a corporation or any subsidiaries as well as any individual who would be subject to the Section 16 reporting rules if the corporation (or any of its subsidiaries) were subject to these reporting rules. This would generally include officers, directors, and 10% shareholders. In the case of a partnership, a specified individual includes any partner that holds more than a 10% equity interest in the partnership and any general partner, officer, or managing partner of the partnership.

- Named Executive Officer. SEC Rules require “clear, concise and understandable” disclosure of all compensation of a company’s named executive officers (CEO, CFO, the three most highly compensated executive officers other than the CEO and CFO and and up to two additional individuals for whom disclosure would have been provided but for the fact that the individual was not serving as an executive officer at the end of the last completed fiscal year). If not publicly traded, this definition is not applicable.

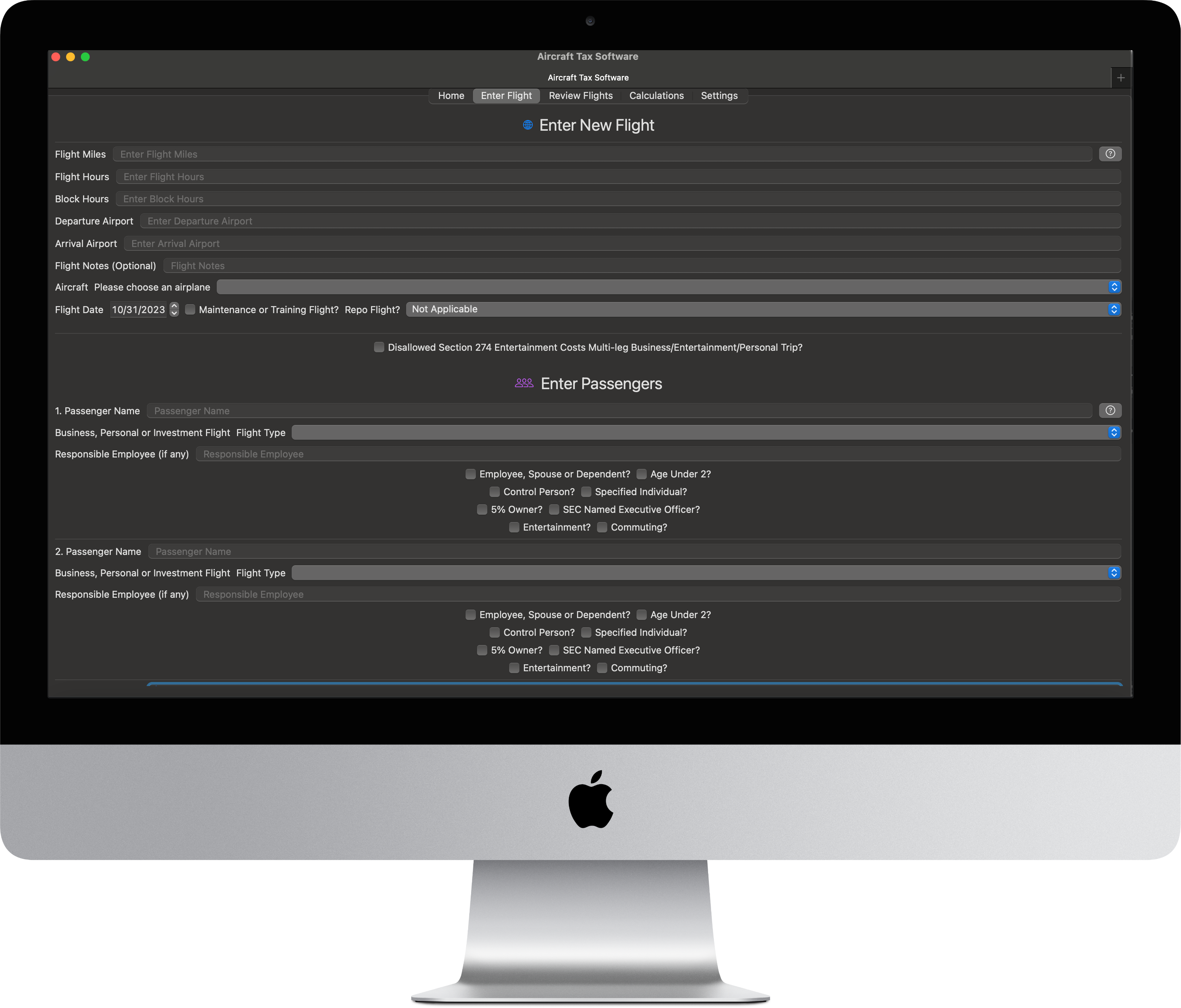

Software User Instructions

At the present time, both web based and MacOS/iOS versions of the Aircraft Tax Software are available. The instructions for use vary slightly. Please see the current user guide.

Uploading CSV Flight Logs

In lieu of entering flight by flight, passenger by passenger information into the software or app, you can upload the data in CSV format. In many cases, you can export data from other flight management software and adjust into CSV format so it can be uploaded. The CSV file imported must conform strictly to the format protocols. Sample CSV files for the web based software can be found under the Upload tabs. For the MacOS software, the following link provides a sample of the proper format.

Multi-State Aircraft Mileage Apportionment

For corporate flight departments and high-net-worth aircraft owners, state and local tax (SALT) compliance now requires granular evidence for income tax apportionment. The traditional "as-the-crow-flies" method is no longer defensible. Our automated geospatial engine uses PostGIS Geodesic Precision and TIGER/Line Statutory Boundaries to ensure every mile is accounted for as the aircraft crosses state lines, including special rules like the "Florida Box." For more details, please see our definitive guide to Multi-State Aircraft Mileage Apportionment.

Sign Up For Free 60 Day Aircraft Tax Software Trial.

Signup for a 60-day free trial of the AircraftTaxSolutions.com Aircraft Tax Software to track personal, entertainment, commuting and business flight hours and miles to compute Internal Revenue Code Section 280F Qualified Business Use percentages, Standard industry fare level (SIFL) imputed income amounts for personal use flights, IRC Section 274 entertainment and commuting expense disallowance amounts and SEC Incremental Costs for reporting for named executive officers. Track Internal Revenue Code Section 280F Qualified Business Use percentage thresholds which must be met or exceeded in the year of purchase to obtain bonus depreciation and to use accelerated depreciation methods, and must be met or exceeded in subsequent years to avoid depreciation recapture. Multi-leg entertainment flight tracking and calculation option included. Repositioning flights tracked. Complete flight package for tax and SEC Aircraft tracking and compliance reporting. Download logs for audit purposes and records. No credit card or commitment needed for 60-day free trial.

Both Web based and MacOS/iOS versions available. All versions (web, Mac, iPhone and iPad) available with a single subscription. Download on the Mac App Store , on the iOS-iPhone App Store or signup for the web version. Sixty-day free trial available (no credit card or commitment required).

* AircraftTaxSolutions.com does not provide tax, legal or accounting advice. These materials have been prepared for informational purposes only, and are not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

About Us

We are a leading financial technology company, which through affiliates, also offers the Domicile365 Tax and Residency Day Count Tracking App.